The Public Service Loan Forgiveness program was created in recognition of the many ways public service workers make our communities and our nation better. The program forgives the remaining balance of federal student debt for public service workers who provide 10 years of public service while making 120 monthly payments.

The PSLF program has forgiven over $78 billion to over 1 million educators and other public service workers. Will you be next?

NEA’s student debt experts have created tools designed to help educators through the PSLF application process. Check them out below!

How Do I Apply for Public Service Loan Forgiveness

PSLF Eligibility

To qualify for PSLF, you must be employed full-time (30 hours or more per week) by a public service employer, which includes all public school districts and public and non-profit higher education institutions. This includes all educators:

- Teachers

- Education Support Professionals and Other School Staff

- Specialized Instructional Support Personnel

- Higher Education Faculty, Including Adjunct/Contingent

The PSLF Application Process

-

Connect with the U.S. Department of Education.

Go to studentaid.gov and login with your Federal Student Aid (FSA) ID (or create one if you do not have one). Your FSA ID provides access to your student debt dashboard, which includes a wealth of historical information on your federal student loans and debt forgiveness opportunities. Make sure your FSA ID contact information is up to date. The Department of Education will use that information to contact you about the progress of your PSLF application. Due to the large-scale reductions in force (RIFs) implemented by the second Trump administration, response times may vary significantly.

-

If you have a FFEL, Perkins, or Parent Plus loan, you must first consolidate into a Direct Loan for your loans to be eligible for forgiveness under PSLF.

Apply for Direct Loan consolidation to combine multiple federal student loans into one loan with a single monthly payment. When you consolidate the Department of Education will calculate an updated PSLF payment count. Learn more about this calculation under the consolidation question in our PSLF FAQ resource.

-

Once you have a Direct Loan you can apply for PSLF.

To benefit from PSLF, the Department of Education recommends submitting the PSLF form every year while you’re making progress toward PSLF. They will use the information you provide on the form to inform you if your employment qualifies and to confirm if you’re making qualifying PSLF payments. Access the Department of Education’s PSLF Help Tool to fill out your PSLF application.

-

Submit your Employment Certification Form (ECF).

To apply for PSLF, the U.S. Department of Education requires public service workers to file an Employment Certification Form (ECF) to show they work for a qualified employer. You can use the Department’s PSLF Help Tool or seek assistance from NEA Member Benefits through our Student Debt Navigator. Note that the ECF must be filled out by an official who can access your employment/service records––usually someone in your human resources department. Some school districts even have an HR person designated to handle ECFs.

Frequently Asked Questions on Public Service Loan Forgiveness

Our experts answered some of the most common questions about Public Service Loan Forgiveness.

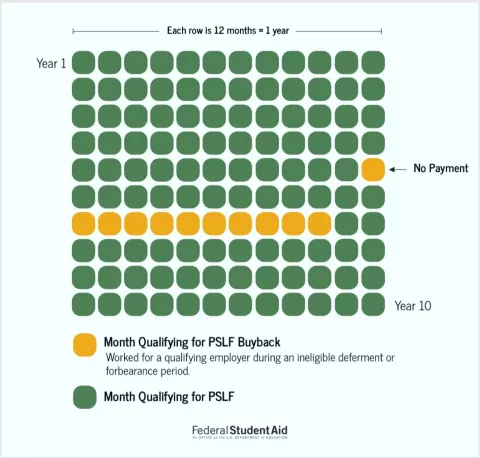

The PSLF Buyback Program

Because of changes in PSLF regulation, borrowers can now “buy back” certain months in their payment history to make them qualifying payments for PSLF. This includes months borrowers were in deferment of forbearance status.

Borrowers can only buy back months if:

- They still have an outstanding balance on their loans;

- They have approved qualifying employment for those same months; and

- Buying back those months would complete the borrower’s total of 120 qualifying PSLF payments.

How Does the PSLF Buyback Program Work?

When buying back months, borrowers must make an extra payment of at least as much as what they would have made under an income-driven repayment (IDR) plan during the months the borrower is trying to buy back. The amount required will be based on the borrower’s income and family size at the time of the deferment or forbearance, not their current income and family size.

If you believe you qualify for Buyback, you can submit a request through PSLF Reconsideration here. In your request, indicate “I am seeking PSLF and have at least 120 months approved of qualifying employment. Please assess my eligibility for PSLF buyback.”

Once you submit a request, you will receive an automated email confirming receipt of your reconsideration request. While borrowers are unable to check the status of their reconsideration request, if you are eligible to buy back months, the U.S. Department of Education should respond within 90 days with a buy back agreement, which will include the amount to pay and instructions for paying the amount.

Due to the large-scale reductions in force (RIFs) implemented by the second Trump Administration, response times may vary significantly.

STORIES OF STUDENT DEBT FORGIVENESS

Did you get your student debt forgiven through Public Service Loan Forgiveness? Help us continue to advocate for this program by sharing how PSLF helped you.